The cannibalizing effect of share buybacks. Are there parallels with Japan’s bubble years?

The following article was originally published in “What I Learned This Week” on November 30, 2017. To learn more about 13D’s investment research, please visit our website.

Consumer advocate Ralph Nader recently delivered a harsh assessment of share buybacks that resonated with us. During a recent CNBC interview, he said: “[Why isn’t] all this capital being spent for productive plant and equipment, or sent back into dividends to increase consumer demand, or shoring up shaky pension plans or going into research and development? When they buy the stock back, when it’s near its high, is a sign of unimaginative or incompetent or avaricious management.” Perhaps Nader’s views are too extreme, but we recall a similar sentiment expressed many years ago by the late Frank Cappiello, a well-known money manager who was a frequent guest on Louis Rukeyser’s Wall Street Week. The point is that when individuals from opposite sides of the political spectrum come to a similar conclusion, then chances are that conclusion contains an element of truth.

General Electric (GE, $18.48) is the latest case in point. As Bloomberg reported in a June 16th article headlined “The $31 Billion Hole in GE’s Balance Sheet That Keeps Growing,” GE spent roughly $45 billion on share repurchases in 2015 and 2016 — at substantially higher stock prices — while a $30 billion- plus shortfall was building in its pension plans. Moreover, during its recent analyst meeting, management disclosed that it would have to borrow money to fund a $6 billion contribution to its pension plans next year, as well as cut its 2018 capex by 26%.

The good news is that GE’s new leadership team recognizes that it has to manage its cash flow more conservatively and realistically, being mindful of an increasingly-challenging business environment. The bad news is that the financial markets may be less accommodating to capital-allocation mistakes in the future.

Consider the challenge of managing pensions in a low-rate environment — a problem that all companies face, not just GE. If interest rates continue rising — as we believe is highly likely — the principal value of the bonds currently held in these pension plans could take a substantial hit, even though they are considered relatively “safe” investments.

One could argue that the financial engineering that has characterized the “free money” era of super-low interest rates has imperiled the longer-run growth potential of the U.S. economy. An interesting parallel can be found in the Japanese experience with corporate cross-shareholdings. This system — an outgrowth of postwar reconstruction — was designed to strengthen business relationships and keep investors around for the long haul, but also had the effect of dissuading activist shareholders and creating a drag on asset efficiency.

A corporate governance code that went into effect two years ago now requires Japanese companies either to reduce their cross-shareholdings or explain why they have not done so. The ratio of cross-shareholdings to total market cap, which had already been on the decline since 1990, has taken another turn downward of late, as shown in the following chart on the left. Before 1990, cross-share-ownership climbed relentlessly, peaking around the same time as the Japanese stock market.

The most interesting dynamic shown in the following charts is that the bull market in the Nikkei since 2012 has accelerated without any help from cross-share-ownership, which lends credence to the view that such ownership arrangements may do more harm than good.

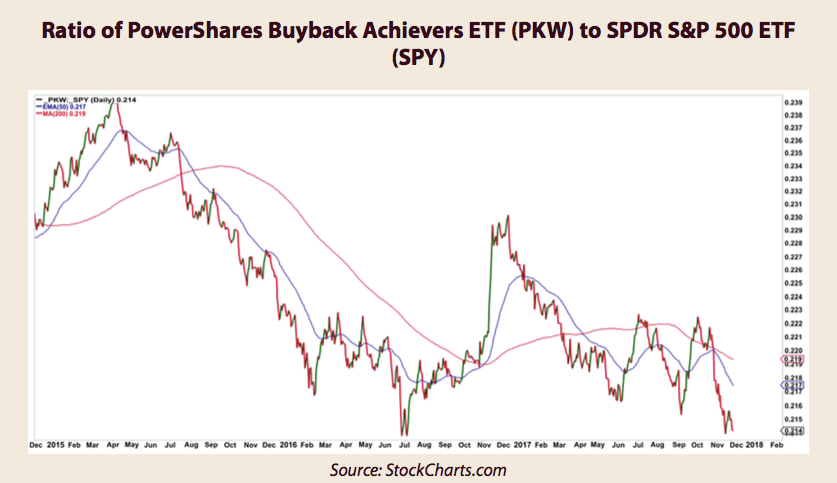

This begs the following question: are companies that purchase too many of their own shares — especially when those shares trade above their “intrinsic value” — also doing more harm than good? One look at the relative performance of the PowerShares Buyback Achievers ETF (PKW, $57.09), shown in the following chart, can provide some insight into the preceding question.

We issued a bearish call on PKW in WILTW July 30, 2015, and, while the ETF’s price has risen marginally since then, its relative strength has been abysmal, and appears perilously close to breaking down below its post-Brexit support level. According to data cited by The Wall Street Journal, PKW has suffered more than $200 billion of outflows since the end of last year.

The Wall Street Journal also recently cited data that S&P 500 companies are repurchasing shares at a rate of roughly $125 billion a quarter this year, which is the lowest level since 2012 and down from an average of $142 billion a quarter between 2014 and 2016.

The following chart portrays an even-more disturbing story, however. While buybacks and dividends-as-a-percent of sales more than doubled from a post- recession low of 3.5% to a high last year of more than 8%, capex-as-a-percent of sales has largely stayed within a narrow range between 4% and 5%, and has not even recovered to its pre-GFC high.

Although the capex share of sales has finally begun to edge upward, some of these companies could find themselves in the lurch if the economy hits a rough patch or the cost of capital moves substantially higher in the months and years ahead. Will these companies suffer from buyer’s remorse after gorging on their own shares at expensive prices when the cost of capital was so low, when they should have been spending on long-lived hard assets?

The ultimate irony is that the companies that did spend heavily on share repurchases when capital was super-abundant may not have enough firepower to purchase shares when another bear market ensues. An article in The Economist dated September 12, 2014, and headlined “The Repurchase Revolution,” remarked on how managements have been terrible predictors of their own share prices:

“Overall, though, executives are hopeless. This is amply illustrated by the fact that buy-backs last peaked in 2007, just before the crash, whereas few firms bought in 2009 when shares were dirt-cheap. In the six months to May 2008, as Lehman Brothers faced a cash crunch that would end in its bankruptcy, it blew $1 billion on buying its shares. In all, America’s financial sector repurchased $207 billion of shares between 2006 and 2008. By 2009 taxpayers had had to inject $250 billion into the banks to save them.”

Despite the evidence arguing against excessive share repurchases, it appears that the new tax legislation promoted by U.S. congressional Republicans will restart the trend — an effective rebuff to the millions of disaffected middle class voters who elected Trump in the hopes of “draining the swamp” of special interests. A November 29th Bloomberg story headlined “Trump’s Tax Promises Undercut by CEO Plans to Reward Investors” elaborated, as follows:

“Major companies including Cisco Systems, Pfizer Inc. and Coca-Cola Co. say they’ll turn over most gains from proposed corporate tax cuts to their shareholders, undercutting President Donald Trump’s promise that his plan will create jobs and boost wages for the middle class.

The president has held fast to his pledge even as top executives’ comments have run counter to it for months. Instead of hiring more workers or raising their pay, many companies say they’ll first increase dividends or buy back their own shares.

Robert Bradway, chief executive of Amgen Inc., said in an Oct. 25 earnings call that the company has been ‘actively returning capital in the form of growing dividend and buyback and I’d expect us to continue that.’ Executives including Coca-Cola CEO James Quincey, Pfizer Chief Financial Officer Frank D’Amelio and Cisco CFO Kelly Kramer have recently made similar statements. ‘We’ll be able to get much more aggressive on the share buyback’ after a tax cut, Kramer said in a Nov. 16 interview.”

This article was originally published in “What I Learned This Week” on November 30, 2017. To subscribe to our weekly newsletter, visit 13D.com or find us on Twitter @WhatILearnedTW.